Getting a $500,000 business loan is achievable but the path can look different depending on your credit profile, time in business, and how quickly you need the funds. This guide walks through what lenders actually look for, which products are available at this loan size, and how to put yourself in the best position before you apply.

Who Qualifies for a $500K Business Loan

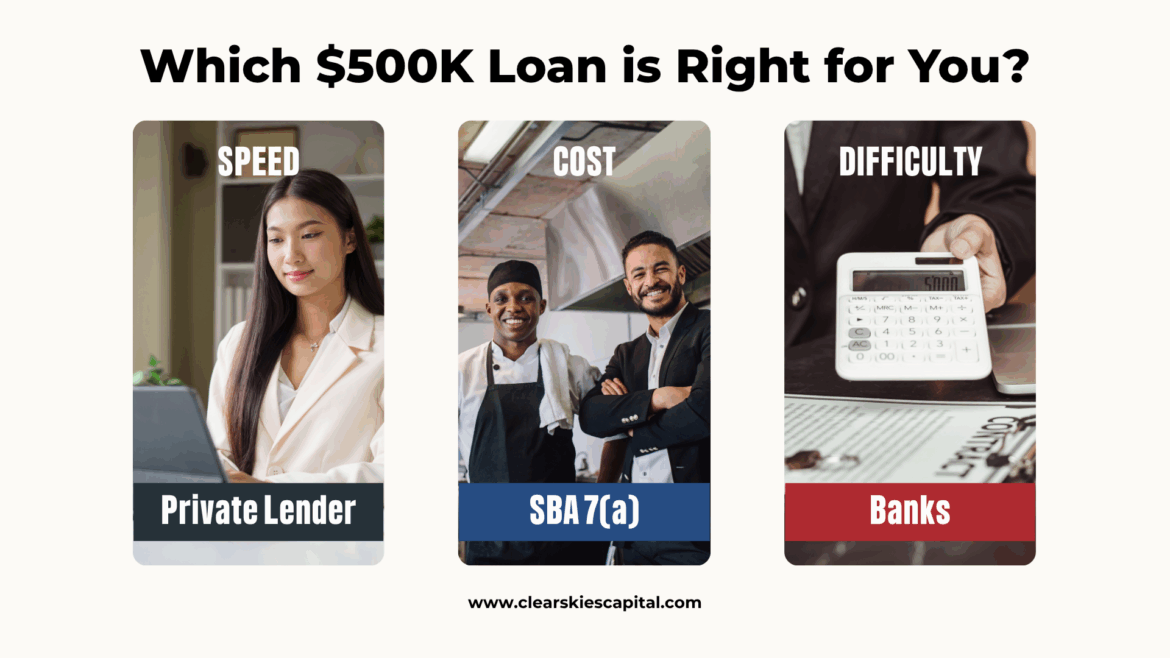

At $500,000, you’re at the upper end of what most alternative lenders offer and squarely in the range of SBA and conventional bank products. Here’s what lenders generally want to see at this loan size:

| Requirement | Traditional Bank | SBA 7(a) | Private Lender |

|---|---|---|---|

| Min. Credit Score | 680+ | 675+ | 500+ |

| Time in Business | 2+ years | 2+ years | 6 months+ |

| Annual Revenue | $500K+ | $300K+ | $120K+ |

| Collateral | Often required | Sometimes required | Not required |

| Funding Speed | 2–8 weeks | 30–90 days | 24–72 hours |

| Max Loan Amount | Varies | Up to $5M | Up to $500K (lump sum) |

The higher the loan amount, the more scrutiny lenders apply to your cash flow, credit, and business stability. That’s not a reason to avoid applying, it’s a reason to understand which lender fits your profile before you spend time on an application that won’t convert.

Loan Products Available at $500K

Not every product is available at every loan size. Here’s what’s realistic at $500,000:

SBA 7(a) Loan

The SBA 7(a) program is the most competitive product available at this size — lower rates, longer terms (up to 25 years for real estate), and government-backed stability. The tradeoff is time. SBA loans take 30–90 days to close and require strong documentation. If you have the runway to wait, this is often the best long-term decision.

Business Term Loan

A lump-sum loan repaid over a fixed term with predictable payments. At $500K, you’ll typically need strong revenue, 1–2 years in business, and clean bank statements. Private lenders can fund this in 24–72 hours with no collateral required for qualified borrowers.

Equipment Financing

If the $500K is earmarked for equipment, this is worth a separate conversation. Equipment financing uses the asset itself as collateral, which typically results in lower rates and more accessible qualification requirements. Terms of 2–5 years are standard.

Revenue-Based Financing

For businesses with strong monthly revenue, revenue-based financing offers up to $1M with flexible repayment tied to cash flow. Approvals in 4 hours or less. No equity dilution. Best for businesses that need capital quickly and have consistent monthly deposits.

What Lenders Actually Look At

Lenders at the $500K level are looking for one thing above everything else: evidence that your business can service this debt while continuing to operate.

| Factor | What It Signals | How to Strengthen It |

|---|---|---|

| Monthly Revenue | Cash flow capacity to repay | Show 6 months of consistent deposits |

| Credit Score | Repayment reliability | Pay down revolving debt, dispute errors |

| Time in Business | Operational stability | 2+ years significantly expands your options |

| Bank Statement Consistency | Revenue stability | Avoid large unexplained gaps or dips |

| Existing Debt | Debt service capacity | Reduce outstanding balances before applying |

| Collateral | Risk mitigation for lender | Real estate or equipment can unlock better terms |

One thing we see consistently: businesses with $500K+ in annual revenue and clean, consistent bank statements qualify more often than businesses with higher revenue but volatile deposits. Consistency matters more than peaks.

Step-by-Step: How to Apply

Step 1 — Know your numbers before you call anyone. Have your last 3–6 months of business bank statements, your most recent tax return, and a clear sense of your monthly revenue. This is the core package every lender will ask for.

Step 2 — Match your profile to the right product. If your credit score is above 650 and you have 2+ years in business — start with SBA. If you need funds in under a week — go to a private lender. If the funds are for equipment — look at equipment financing specifically. Don’t apply for a product that doesn’t fit your profile.

Step 3 — Apply with a single lender first. Multiple simultaneous applications can trigger hard credit pulls that lower your score and signal desperation to underwriters. Start with the lender that best fits your profile, get a decision, then evaluate.

Step 4 — Review the total repayment amount, not just the rate. Before signing anything, ask your lender: what is the total dollar amount I will repay over the life of this loan? That number — not the stated interest rate or APR — is your true cost of capital.

Step 5 — Understand the payment structure. Daily, weekly, or monthly payments affect your cash flow differently. Make sure the payment frequency aligns with how your business actually receives revenue.

A Simple Example

Business: HVAC company, $800K/month in revenue, 3 years in operation, 640 credit score

Goal: $500,000 to expand into a second market

↓

Option A — SBA 7(a): ~11–13% rate, 10-year term, $5,500/month payment, 60-day close

Option B — Business Term Loan: 18–28% rate, 3-year term, faster to fund, higher monthly payment

↓

Decision: With a 60-day runway and 640 credit, SBA is the right call. With a 2-week deadline and the same profile, the term loan bridges the gap.

The right answer depends on your timeline as much as your credit.

Common Mistakes to Avoid

- Applying at too many places at once — can hurt your credit if the lender you are working with requires a hard credit pull.

- Not having bank statements ready — slows every application by days

- Focusing only on the interest rate — total repayment amount is the number that matters

- Underestimating time in business requirements — if you are under 1 year in business, a revenue-based financing option may be better suited to start with.

- Ignoring prepayment terms — some lenders penalize early payoff; others offer discounts

Frequently Asked Questions

Can I get a $500K business loan with bad credit?

Yes, though your options narrow. Alternative lenders like Clear Skies Capital work with scores as low as 500. At that credit level, revenue consistency and time in business carry more weight. Expect higher rates than you’d see with a 680+ score.

How hard is it to get a $500,000 business loan?

It depends on how your file looks. If you’re an established business with strong, consistent revenue, getting approved for $500K can be relatively straightforward. If your business is newer or doing lower monthly sales, the path to $500K may take more time or come in smaller pieces.

Do I need collateral for a $500K business loan?

Not always. SBA loans sometimes require it. Most private lenders do not require collateral for term loans up to $500K for qualified borrowers.

How much down payment for a $500,000 business loan?

It depends on the type of lender. Most private lenders don’t require a down payment for non-SBA products. Instead, they charge an origination fee, which is often deducted from the total amount you receive. Traditional banks typically don’t require a down payment either, but they may charge smaller fees and have stricter approval requirements.

How long does it take to get $500K?

It depends entirely on the product. Private lenders can fund in 24–72 hours. SBA loans take 30–90 days. Banks fall somewhere in between. Have your documents ready before you apply — that’s the single fastest thing you can do to accelerate any timeline.

What revenue do I need to qualify?

At Clear Skies Capital, we work with businesses generating $120K+ annually ($10K/month). For a $500K loan specifically, most lenders want to see monthly deposits that comfortably cover the projected payment with room to spare.

What are the risks of a small business loan?

One of the biggest risks is the personal guarantee. If your business can’t repay the loan under the agreed terms, you may be personally responsible for the balance. That can put your personal bank accounts or assets at risk.

How much is the monthly payment on a $50,000 business loan?

Monthly payments can range from around $1,000 to over $2,000, depending on your rate, term, and lender. For example, a $50,000 loan over 5 years at 7% interest is about $990 per month. Shorter terms or higher rates can push payments well above $2,000.

What disqualifies you from a small business loan?

The most common reasons include poor credit, limited time in business, and past defaults on government-backed loans. Lenders may also decline applications due to inconsistent revenue, weak cash flow, or too much existing debt.

Ready to See What You Qualify For?

We work with businesses at every stage to find the right fit — whether that’s a direct term loan, an SBA product, or a combination that gets you where you need to go.

Call 1-800-230-9822 or apply online at clearskiescapital.com.

No obligation. No impact to your credit score.

Rates are for informational purposes only and reflect general market conditions as of April 2026. Actual rates vary by lender, business profile, and creditworthiness. Not available in all states.

Glossary

| Term | Simple Definition |

|---|---|

| SBA 7(a) Loan | A government-backed small business loan partially guaranteed by the U.S. Small Business Administration, known for offering competitive rates and long terms. |

| Business Term Loan | A lump-sum loan provided to a business that is repaid over a fixed term with predictable, scheduled payments. |

| Equipment Financing | A type of business loan used specifically to purchase equipment, where the asset itself serves as collateral for the loan. |

| Revenue-Based Financing | A funding structure where a business receives upfront capital and repays it as a fixed percentage of its ongoing business revenue. |

| Collateral | Physical assets (like real estate or equipment) pledged to a lender to secure a loan, reducing the lender’s risk. |

| Origination Fee | An upfront fee charged by a lender to process a new loan application, typically deducted from the total loan proceeds before they are deposited. |

| Personal Guarantee | A borrower’s legal commitment to repay a business loan using their personal assets if the business fails to make payments. |

| Credit Score (FICO) | A three-digit number that indicates a borrower’s creditworthiness based on their past debt repayment history, used by lenders to assess risk. |