A $100,000 business loan is one of the most common funding requests we see — and one of the most accessible. Unlike larger loan amounts that require years of operating history and pristine credit, $100K is achievable for businesses that are still building their financial profile. If you have 6 months in business and consistent monthly revenue, this is a realistic target.

Key Takeaways

- Revenue Outweighs Credit History: For a $100K loan, lenders prioritize consistent monthly deposits (ideally $15K–$20K+) and at least 6 months in business over a perfect credit score, making this amount accessible even with scores as low as 500.

- The 10–15% “Safety Rule”: To ensure the debt is serviceable, your monthly loan payment should not exceed 10–15% of your gross monthly revenue; for example, a business making $60K/month can comfortably handle a $4,500–$5,500 payment.

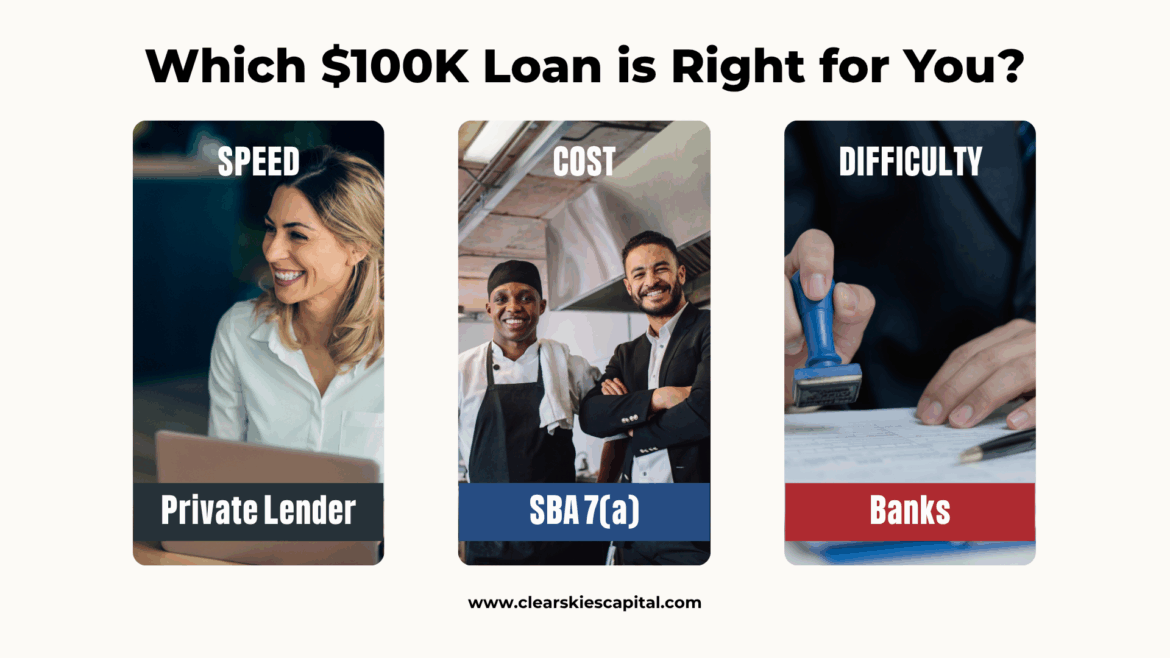

- Speed vs. Cost Strategy: While Private Lenders can fund in as little as 24 hours, SBA 7(a) loans offer the lowest long-term rates but require 2+ years in business and a significantly longer application process.

Is $100K the Right Amount for Your Business?

Before applying, it’s worth asking whether $100K is the right number. Borrowing more than you need increases your payment and your cost. Borrowing less than you need means coming back to the market sooner, which can be harder the second time.

A general rule: your projected monthly loan payment should not exceed 10–15% of your average monthly revenue. At $100K, here’s what typical payments look like:

| Term Length | Estimated Monthly Payment | Min. Monthly Revenue Needed |

|---|---|---|

| 12 months | $9,000–$11,000 | $65,000+ |

| 18 months | $6,500–$8,000 | $50,000+ |

| 24 months | $5,000–$6,500 | $40,000+ |

| 36 months | $3,500–$5,000 | $30,000+ |

These are estimates based on typical alternative lending rates. SBA and bank products will show lower payments at the same amount due to longer terms and lower rates.

Who Qualifies for a $100K Business Loan?

At $100,000, qualification requirements are meaningfully more accessible than at higher loan amounts. More lenders compete for this business, and the bar is lower across the board.

| Requirement | Traditional Bank | SBA 7(a) | Private Lender |

|---|---|---|---|

| Min. Credit Score | 680+ | 650+ | 500+ |

| Time in Business | 2+ years | 2+ years | 6 months+ |

| Annual Revenue | $150K+ | $120K+ | $120K+ |

| Collateral | Often required | Sometimes required | Not required |

| Funding Speed | 2–8 weeks | 30–90 days | 24–72 hours |

The primary difference between $100K and $500K qualification: at $100K, revenue consistency matters more than credit score, and time in business requirements are more flexible. A business with 8 months of operation and $15,000 in consistent monthly deposits can realistically qualify here. That same business would struggle at $500K.

Which Loan Product Is Right at $100K

The right product depends on what you need the money for and how you plan to repay it — not just on the dollar amount.

Business Line of Credit

The most flexible option at this size. Draw up to $250K as needed, pay interest only on what you use, and repay on your own schedule. Best for businesses with ongoing or unpredictable cash flow needs — covering payroll gaps, purchasing inventory, or bridging seasonal slow periods. Funds available in 24 hours or less with no maintenance fees.

Business Term Loan

A lump sum repaid over a fixed term with predictable payments. Best when you have a specific, defined use for the funds — a piece of equipment, a renovation, hiring, or a large contract requiring upfront costs. No collateral required for qualified borrowers.

Revenue-Based Financing

Funding based on your monthly revenue rather than your credit score. Best for businesses with strong monthly deposits that want repayment tied to performance rather than a fixed calendar. Approvals in 24 hours or less.

Equipment Financing

If the $100K is specifically for equipment, apply for equipment financing rather than a general term loan. The equipment itself serves as collateral, which opens up better rates and easier qualification.

SBA 7(a) Loan

Available at $100K but may be more process than the situation requires. If you have 2+ years in business, a 650+ credit score, and don’t need funding in under two weeks, SBA is worth pursuing for the rate alone. If your timeline is tight or your credit is still building, a direct private lender is the more practical path, and a natural bridge to SBA later.

What Do Lenders Look At for a $100K Loan?

At this loan size, three factors carry the most weight:

| Factor | What It Signals | How to Strengthen It |

|---|---|---|

| Monthly Revenue | Can your business service this debt? | Show 3–6 months of consistent deposits |

| Bank Statement Consistency | Is revenue stable or volatile? | Avoid large unexplained gaps between deposits |

| Time in Business | Operational stability and survival risk | Every additional month helps; 12+ months opens more doors |

| Credit Score (FICO) | Repayment reliability | Pay down revolving balances, dispute errors |

| Existing Debt | Remaining cash flow capacity | Reduce outstanding balances before applying |

One pattern we see constantly: businesses with $12,000–$15,000 in monthly deposits and clean, consistent bank statements qualify at $100K even when their credit score is in the 540–580 range. Revenue tells the story that credit can’t always tell on its own.

Step-by-Step: How to Apply

Step 1: Prep Your Financial Proof

Gather your last 4 months of business bank statements and calculate your average monthly deposits. If your average is $50,000+, you are in a strong position to qualify for a $100K loan.

Step 2: Match Your Profile to the Right Lender

- Don’t guess where to apply. If you need speed or have lower credit, go with a Private Lender. If you have 2+ years in business and 650+ credit, start with the SBA.

Step 3: Define Your Goal and Check the “True Cost”

- Be specific about your “Use of Funds” (e.g., “hiring two crews”) to build lender trust. Before signing, ignore the APR and look at the total payback amount to understand the actual dollar cost of the capital.

Ready to See What You Qualify For?

If you’ve been in business for at least 6 months and make $20,000+ per month, you may qualify for up to $100K.

We’ll show you your funding options, cost, and best-fit loan.

Apply at ClearSkiesCapital.com or call 1-800-230-9822.

Practical Scenario: The Path to $100K

Business: Landscaping company, $60,000/month in revenue 14 months in operation, 575 owner credit score

Goal: $100,000 to hire two crews and take on commercial contracts

↓

Best fit: Revenue-Based Financing Funding, 24-month term

Why: 575 credit with 14 months in business and consistent $60K/month deposits qualifies with a direct private lender — not yet at SBA threshold

↓

Estimated monthly payment: $4,500–$5,500

↓

18 months later: 32 months in business, credit improved to 640+ Path to SBA 7(a) refinance opens up

How Your Business Income Affects Your Loan Size

| Profile | Est. Max Funding | Best Product |

|---|---|---|

| 680+ credit, 2+ years, $100K+/month | $100K – $500K | SBA 7(a) or Term Loan |

| 620–679 credit, 1+ year, $60K+/month | $60K – $150K | Term Loan or Line of Credit |

| 550–619 credit, 6+ months, $50K+/month | $40K – $60K | Term Loan or Revenue-Based Financing |

| 500-550 credit, 6+ months, $40K+/month | $30K – $40K | Revenue-Based Financing |

These are ranges, not guarantees. Strong, consistent revenue moves you toward the lower end. Volatile deposits or high existing debt push you toward the higher end regardless of credit score.

Common Mistakes to Avoid

- Applying at multiple lenders simultaneously — can damage your credit if hard pulls are required.

- Not having bank statements ready — the single most common reason applications take longer than they need to.

- Requesting more capital than your cash flow can support — the payment has to work within your monthly revenue, not just your projected revenue.

- Focusing on rate instead of total repayment — a lower rate on a longer term can cost more than a higher rate on a shorter one.

- Ignoring payment frequency — daily or weekly payment products affect your cash flow very differently than monthly. Confirm this before signing.

Get Your $100K Funding Quote in Minutes

If you’re in the market for a $100,000 business loan, we’ve got you covered.

Apply at ClearSkiesCapital.com or call 1-800-230-9822.

Frequently Asked Questions

Can I get a $100K business loan with bad credit?

- Yes. We work with scores as low as 500. At lower credit scores, your revenue consistency and time in business carry more weight than the score itself. The tradeoff is a higher rate — but if the use of funds generates more than the cost of the loan, it can still be the right decision.

Can a new business get a $100K loan?

- With 6 months in business and $10,000+ in monthly deposits, yes. Most private lenders work with businesses as young as 6 months. Under 6 months is very difficult regardless of revenue. If you’re not there yet, the most productive thing you can do is open a dedicated business bank account and build 6 months of clean deposit history.

How hard is it to get a $100,000 business loan?

- Difficulty depends on your credit, revenue, and how quickly you need funds. Bank loans at this size have stricter requirements; online lenders can move faster with more flexible criteria, though at higher rates.

Is it easier to get a loan through an LLC?

- The LLC structure itself doesn’t make approval easier — lenders focus on your business financials, time in business, and credit profile regardless of how you’re incorporated.

Do I need collateral for a $100K business loan?

- Most private lenders don’t require collateral for term loans and lines of credit at this size. Equipment financing uses the equipment itself. SBA loans sometimes require it depending on the deal structure.

How fast can I get $100K?

- As fast as 24 hours with a direct private lender for qualified applicants. Have your bank statements ready before you call — that’s what drives the timeline more than anything else.

Is a line of credit or a term loan better at $100K?

- If you have a specific, one-time use for the funds — term loan. If you need ongoing flexibility to draw and repay as needed — line of credit. Lines of credit also tend to cost less overall if you don’t use the full amount, since you only pay interest on what you draw.

How much is the monthly payment on a $100,000 business loan?

- It depends on your rate and term — a loan calculator is the fastest way to estimate. As a general rule, the shorter the term and the higher the rate, the larger your monthly payment.

What if I’ve been declined before?

- A decline at one lender is not a verdict. Different lenders weigh factors differently. If you’ve been declined, ask specifically why — that feedback tells you exactly what to address before applying elsewhere. Revenue, time in business, and existing debt load are the most common fixable reasons for decline at $100K.

What disqualifies you from a $100K business loan?

- The most common reasons are prior defaults on government-backed loans, less than 6 months in business, and monthly revenue that doesn’t support the projected payment. Inconsistent deposits — even on strong annual revenue — are a more common disqualifier than most business owners expect.

What is considered a good interest rate on a business loan?

- For most businesses, anything below 10% is strong. Bank and SBA loans typically offer the most competitive rates for qualified borrowers.

Can a new business get a $100K loan reddit?

- If you’re under 6 months in business with no revenue, the answer is almost always no. If you’re at 6+ months with $20K+ in monthly deposits, $100K is realistic through private lenders, even with a credit score as low as 500.

Glossary

| Term | Definition |

|---|---|

| Business Line of Credit | A revolving credit facility that lets you draw funds up to a set limit and pay interest only on what you use. Replenishes as you repay. |

| Business Term Loan | A lump-sum loan repaid over a fixed period with scheduled payments. Best for specific, defined uses of capital. |

| Revenue-Based Financing | Funding is repaid as a percentage of monthly revenue rather than a fixed payment. |

| Equipment Financing | A loan used specifically to purchase business equipment, where the equipment itself serves as collateral. |

| SBA 7(a) Loan | A government-backed small business loan partially guaranteed by the U.S. Small Business Administration. Offers competitive rates and long repayment terms. |

| Origination Fee | An upfront fee charged by the lender to process and fund the loan, typically deducted from the loan proceeds at funding. |

| Personal Guarantee | A borrower’s legal commitment to repay the loan using personal assets if the business fails to make payments. |

| FICO Score | A three-digit personal credit score used by lenders to assess repayment reliability. Ranges from 300 to 850. |

| Collateral | An asset pledged to a lender to secure a loan. Lender can claim the asset if the borrower defaults. |

| Total Repayment Amount | The complete dollar amount repaid over the life of a loan, including all interest and fees. The most reliable way to compare loan costs across different products. |

| Debt Service Coverage Ratio (DSCR) | A measure of whether a business generates enough cash flow to cover its loan payments. Calculated by dividing net operating income by total debt payments. |

| Hard Credit Pull | A formal credit inquiry that appears on your credit report and can slightly lower your score. Typically happens at final approval, not pre-qualification. |